June 2026 Investment Update: These Are Not Synonyms: Information & Signal

May 29, 2026

"The problem with experts is that they do not know what they do not know."

—Nassim Taleb

Most investors today do not suffer from a lack of information. They suffer from too much of it.

Headlines arrive instantly. Opinions multiply by the minute. Every economic release, policy debate, and geopolitical development gets dissected in real time across an expanding number of channels.

The question is no longer where to find market commentary but which commentary or opinion, if any, deserves a response.

The month of May was a useful illustration. Markets navigated inflation concerns, shifting rate expectations, geopolitical tension, fiscal debates, and ongoing questions about artificial intelligence and concentration risk. Underlying trends largely persisted through the noise. The gap between what headlines suggested and what markets actually did was notable, though not unusual.

This month's Note explores the distinction between information and signal, why short-term activity often feels more important than it is, and how a systematic investing process helps separate temporary noise from lasting change.

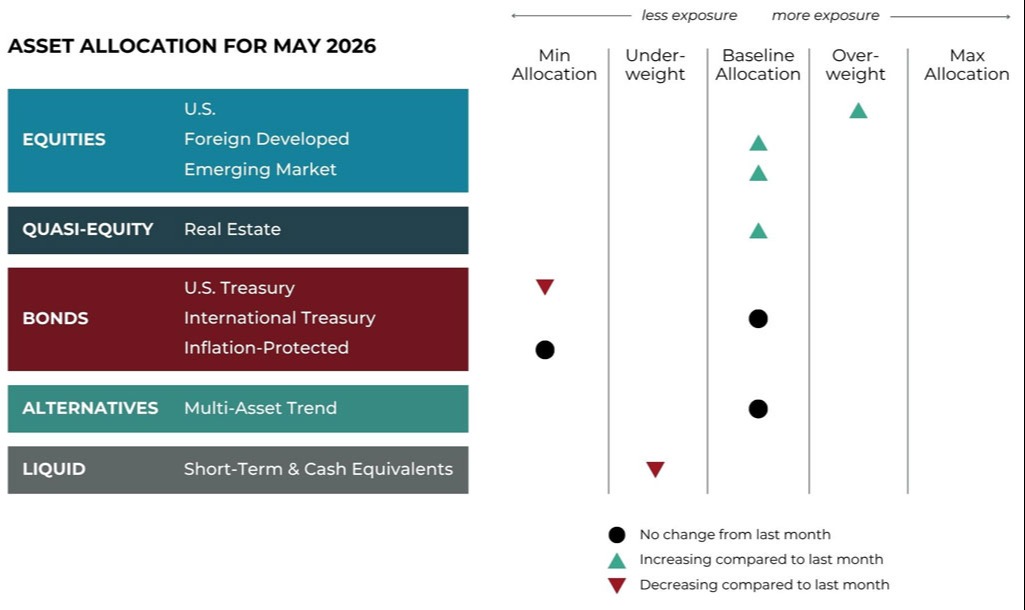

But first, here’s a summary of the global asset classes utilized in our portfolios and their exposures for June.

Asset Allocation Update

Source: Blueprint Investment Partners

Adjustments can vary across strategies depending on each strategy's objectives. What's illustrated above most closely reflects allocation adjustments for the Growth Strategy. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility.

U.S. Equities

Exposure will not change and remain overweight. Both the intermediate-term and long-term trends are positive.

International Equities

Exposure will not change and remain at baseline. Both foreign developed and emerging market equities have intermediate- and long-term uptrends.

Real Estate

Exposure will remain at its baseline allocation as trends over both timeframes remain positive.

U.S. & International Treasuries

International Treasuries are now being partially expressed with an adaptive fixed income ETF. This will allow for continued baseline exposure and offer the ability to potentially benefit from both positive and negative trends. U.S. Treasuries of medium to long duration remain in downtrends across all timeframes and will continue to be underweight.

Inflation-Protected Bonds

Exposure will remain at its minimum as this asset group continues to be weaker than other fixed income assets.

Alternatives

Exposure is expressed through a multi-asset alternative ETF. Fixed income continues to have the largest net exposure (short prices, long rates). Net long equities remains in the second spot as the largest long position. International currencies and commodities round out the exposure, with both continuing to be net long.

Short-Term Fixed Income

Exposure will not change and be overweight as this asset class continues to hold allocations from weaker fixed-income instruments.

Asset-Level Overview

Equities & Real Estate

Uncertainty in the Middle East, energy prices, and inflation remain the dominant factors impacting equity markets. Despite these risks, the S&P 500 moved higher in May, expanding on April’s rally and making new all-time highs once again. The result is that trends remain positive and our portfolios will continue to be overweight.

International equities were more mixed in May, with developed markets joining U.S. markets moving higher and emerging markets trailing the other two. This divergence has allowed U.S. performance to close the gap year-to-date, but international equities continue to outperform. Trends remain solidly positive, which will allow our portfolios to maintain their current allocations.

Real estate security returns were on the muted side in May, with performance currently sitting slightly positive for the month. With renewed inflation concerns pushing lending rates higher, this segment is facing a significant headwind. A new Federal Reserve Chair is yet another factor contributing to uncertainty for this asset class.

Fixed Income & Alternatives

Speaking of asset classes affected by inflation and monetary policy uncertainty, fixed income instruments continued to mostly struggle in May. Pressure on rates to rise has driven bond prices lower across all durations. The result is that our portfolios will remain at their minimum allocations in favor of money market instruments.

Within the alternatives allocation very little change has occurred as we transition to June. Sustained equity trends will keep the equity allocation high while interest rate support described above will keep major short positions in place for fixed income instruments. Elevated oil prices will once again hold the commodity allocation net long while the net long to international currencies will be virtually unchanged.

Sourcing in this section: fortune.com, “S&P 500 sets all-time high, welcomes another company to $1 trillion market cap club,” 5/27/2026

3 Potential Catalysts For Trend Changes

Inflation Rising: The Fed’s preferred gauge of monthly price increases grew more slowly in April. However, it remained higher than the Fed’s ideal target. The personal-consumption expenditures (PCE) price index rose 0.4% in April versus the previous month, and it rose 0.7% in March. During the past year, the index increased 3.8%, which is higher than the Fed's 2% target. The core 12-month PCE inflation rate is 3.3%. Compared to a year ago, energy prices rose 18%, gasoline 28%, fuel oil 54%, and airfare prices 21%. The latest report means that the rate cuts the market expected at the start of the year are no longer a 2026 story. Four months ago, the Federal Reserve was considering whether to keep cutting interest rates to help a shaky labor market. Now, with inflation data being so critical, the Fed’s policy debate has shifted from when to cut rates to when to signal that a rate hike is as likely as a rate cut.

Consumer Confusion: Consumers are the cornerstone of the American economy. So far, their spending has held up well in 2026 despite higher prices and slow labor-market hiring. For example, retail sales grew by 0.5% in April. Yet, in economic surveys, Americans report one of the grimmest moods on record. On the other hand, the stock market doesn't seem to be reflecting a sour outlook. Last week, the S&P 500 logged its eighth-consecutive week higher.

Ongoing Housing Squeeze: U.S. home-price growth slowed slightly in March, during a time when higher mortgage rates intensified the affordability squeeze for home buyers. A measure of home prices across the country, S&P Case-Shiller National Home Price Index, increased 0.7% in the 12 months through March versus a 0.8% rise in February. Mortgage rates also recently hit the highest level since August (6.51% for a 30-year fixed). Mortgage rates usually loosely track 10-year Treasury yields, which have risen following high inflation data. The combination of prices, rates, and other factors spells bad news for home shoppers and coincides with what is usually the busiest time of year for home sales. A fourth-straight slow year for the housing market will also be a challenge for industries that rely on home sales, such as real-estate brokerages, mortgage lenders, home builders, and furniture manufacturers.

Sourcing for this section: The Wall Street Journal, “Iran War Keeps Fed’s Inflation Gauge Above Inflation Target,” 5/28/2026; The Wall Street Journal, “Inflation Soared to 3.8% in April, Driven by Gasoline Prices,” 5/12/2026; The Wall Street Journal, “Retailers’ Sales Growth Cooled Last Month,” 5/14/2026; finance.yahoo.com, “S&P 500 eyes 8th straight weekly gain amid Iran deal hopes,” 5/22/206; The Wall Street Journal, “U.S. Home Price Growth Slowed in March,” 5/26/2026; and The Wall Street Journal, “Mortgage Rates Hit a Nine-Month High in Blow to Prime Buying Season,” 5/21/2026

Information is Flowing Faster, But Trends Usually Are Not

In the short run, the market is a voting machine but in the long run it is a weighing machine.”

– Benjamin Graham

If you followed financial headlines during May, you would be forgiven for thinking markets had every reason to struggle. Investors navigated persistent inflation concerns, shifting expectations around interest rates, geopolitical uncertainty, fiscal debates, questions surrounding global growth, and the constant drumbeat of election-related noise around the world. On top of that, developments in artificial intelligence continued creating excitement in some corners of the market while simultaneously raising concerns about concentration risk and valuations in others.

The modern investor has access to more information than at any point in history. News alerts arrive instantly. Market commentary appears by the minute. Social media amplifies every opinion, prediction, and short-term market move. Information moves faster than ever before. The interesting thing is that trends generally do not.

One of the core principles behind systematic trend following is recognizing that markets often experience temporary volatility (both up and down) without experiencing a meaningful change in direction. A sharp move over several trading sessions may feel important at the moment. A concerning headline may create anxiety. An unexpected economic report may dominate conversations for days. But short-term activity and long-term trend change are not always the same thing.

Investors frequently face a difficult behavioral challenge: separating information from noise. When headlines arrive continuously, it becomes tempting to react continuously. Yet history has repeatedly shown that frequent reactions can create more problems than they solve. As the quote above from legendary investor Benjamin Graham observes: daily sentiment, emotion, and headlines can influence short-term outcomes, but sustained trends tend to reflect larger underlying forces over time.

This distinction matters because successful investing is not simply about gathering information. It is about identifying which information deserves action. Trend following does not attempt to predict inflation readings, forecast central bank decisions, estimate election outcomes, or anticipate geopolitical developments. Those variables matter, but markets often process them long before consensus opinion catches up.

Instead, systematic trend following focuses on a different set of questions:

- What is happening?

- Is it persistent?

- Does portfolio positioning need to adapt?

That discipline becomes especially valuable during environments like today, where information flow can create the illusion that every development requires immediate action. Sometimes trends change quickly. Risk management exists for precisely that reason. But many times, markets demonstrate resilience even while headlines suggest instability. Strong trends can persist longer than investors expect. Weak trends can deteriorate further than forecasts predict.

Our systematic investing process exists to reduce the temptation to confuse motion with direction. Headlines will continue moving faster than trends. They generally always have. The goal is not to ignore information. The goal is to maintain the discipline to distinguish between temporary noise and lasting change. Because over time, successful investing is often less about reacting faster and more about reacting better.

May 2026 Investment Update:

A Disconnect Between Headlines & Market Behavior.

April 30, 2026

"The greatest liberty is born of the greatest rigor."

—Paul Valéry

The market environment over the past several weeks has been defined by speed. A sharp equity drawdown was followed by an equally rapid recovery, creating a difficult backdrop for many investors and particularly for systematic investing strategies.

In periods like this, price tends to move faster than fundamentals can be interpreted or acted upon. By the time a narrative takes shape, markets have often already moved in the opposite direction.

Moves like these can feel disorienting, as conditions change faster than most investing approaches are designed to fully capture. They also tend to expose the tradeoffs embedded in different approaches — especially those that rely on price and discipline rather than prediction.

This month’s investment update examines how our trend-following process has evolved to better navigate these environments and how those refinements influenced positioning through the recent volatility.

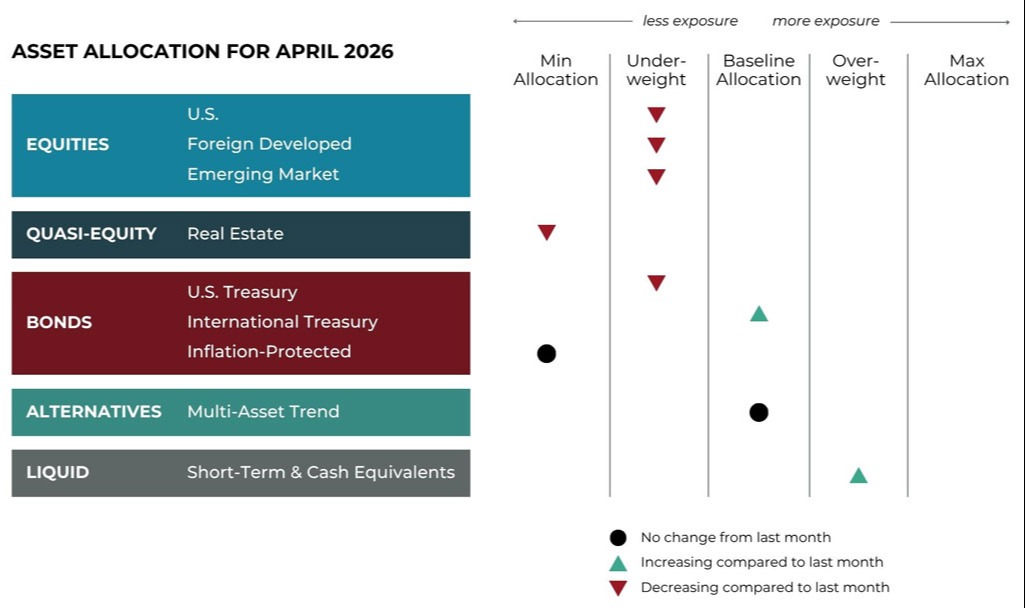

But first, here’s a summary of the global asset classes utilized in our portfolios and their exposures for May.

Asset Allocation Update

Source: Blueprint Investment Partners

Adjustments can vary across strategies depending on each strategy's objectives. What's illustrated above most closely reflects allocation adjustments for the Growth Strategy. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility.

U.S. Equities

Exposure will increase and move to overweight. The intermediate-term trend has resumed its positive direction, joining the long-term trend.

International Equities

Exposure will increase to baseline. Both foreign developed and emerging market equities have intermediate-term uptrends. Trends continue to be positive over the long-term timeframe as well.

Real Estate

Exposure will increase back to its baseline allocation as trends over both timeframes revert to positive.

U.S. & International Treasuries

International Treasuries are now being partially expressed with an adaptive fixed income ETF. This will allow for continued baseline exposure and offer the ability to potentially benefit from both positive and negative trends. However, U.S. Treasuries of medium to long duration continue to experience downtrends over both timeframes and will remain underweight.

Inflation-Protected Bonds

Exposure will remain at its minimum as it continues to be weaker than other fixed income assets.

Alternatives

Exposure is expressed through a multi-asset alternative ETF and is overall little changed heading into May. Fixed income will continue to have the largest net exposure (short prices, long rates). Net long equities remain in the second spot and is the largest long position. International currencies and commodities will again bring up the rear in terms of exposure, with both continuing to be net long.

Short-Term Fixed Income

Exposure will decrease to underweight as exposure is returned to strengthening equities.

Asset-Level Overview

Equities & Real Estate

While no sustainable solution has been reached yet, the temporary ceasefire and its subsequent extension in Iran has been the catalyst for a massive rally in equities back to new highs within the span of just a couple weeks. As we mentioned in last month’s update, an otherwise strong economy is likely providing the foundation for a continuation of positive trends once uncertainty in the Middle East abates. This appears to be the case thus far as April draws to a close.

International equities have also benefited from the temporary cooling of tensions as negotiations continue. Productive discussions mean lower oil prices, which means less pressure on inflation to continue. This in turn opens the door for favorable monetary policy.

Last but not least to benefit from the temporary ceasefire are real estate securities. Like their other equity counterparts, the hint of stable interest rates have allowed them to resume the uptrends they had started going into April.

The result is that our portfolios will increase exposure in all these areas.

Fixed Income & Alternatives

Many of the same catalysts driving equity markets are also influencing fixed income, albeit in different ways. After the prospect of a spike in inflation drove rates higher and prices lower, a pause in the intensity of the war has allowed prices to stabilize. Interestingly, bond prices have not recovered anywhere near what equity prices have; in some cases they have been flat to lower. This raises the question of what else is driving bond markets. Perhaps it is the grilling of the new Fed Chair candidate? Who knows, but for now prices remain weak enough that no new uptrends have emerged.

Within the alternatives allocation, the recovery in equity prices will keep the equity allocation high. Elevated oil prices will keep the commodity allocation net long while the net long to international currencies will be subdued. Last but not least, the fixed income allocation will continue to be net short but poised to change quickly if bond prices recover.

3 Potential Catalysts For Trend Changes

Sentiment Matters: Concerns about the war in Iran have led Americans to their most pessimistic economic outlook on record, according to the University of Michigan’s long-running consumer sentiment survey. The index fell to 49.8 in May from 53.3 in April, below the previous record low of 50 set in June 2022. A preliminary April reading of 47.6 had already indicated worsening sentiment. Notably, Americans now feel worse about the economy than during the COVID-19 pandemic, the 2008-2009 Financial Crisis, or the high inflation period of the late 1970s. Despite this pessimism, consumer spending has remained relatively stable. While April data is pending, March retail sales were strong, and major banks report that household finances are solid. As for unemployment expectations, which economists have tracked since the 1960s, pessimism during the past year has risen and matched levels typically seen only during recessions. In March, both the New York Fed and the Conference Board reported increased consumer negative sentiment. An April poll by the Associated Press-NORC Center for Public Affairs Research found that 73% of Americans believe the economy is performing poorly. Never before have so many expected unemployment to rise without an actual recession. This unusual labor market likely reflects limited hiring and firing, fewer available workers due to immigration restrictions, and uncertainty about the effects of artificial intelligence.

Pricing Expectations: The Labor Department reported that consumer prices rose 3.3% in March compared to a year earlier, up from 2.4% in February. This is the highest inflation rate in two years, though it met economists’ expectations. At his final Federal Reserve meeting as Chairman, Jerome Powell cautioned that inflation is likely to continue rising in the coming months. “It hasn’t even peaked yet,” Powell stated at a press conference on Wednesday. “There’s headline inflation coming out of the Gulf, and we don’t know how much that will be.” Core inflation, which excludes food and energy, increased by 2.6%, just below the 2.7% forecast. Consumers are reducing purchases in categories with the largest price increases, indicating that company price hikes, rather than strong demand, are driving inflation. While Americans continue to spend, aided by tax refunds, their purchasing patterns are shifting. Spending on clothing, furniture, and sports equipment has declined as these items have become more expensive, while spending on services and experiences, such as travel and healthcare, has increased. Bureau of Economic Analysis data through February shows that inflation-adjusted spending is falling most for goods with the highest price increases. Overall, consumer spending remains steady, suggesting inflation’s impact may be limited, even as many express concern.

Powell’s Last Dance: For 75 years, every Federal Reserve Chair has left the central bank when a successor was appointed. Powell has broken this tradition by announcing he will remain on the Fed’s board as a Governor after transferring leadership to Kevin Warsh in May. This decision reflects the significant influence of the President Donald Trump administration on the Fed’s operations. Powell’s announcement followed a criminal investigation into his management of building renovations, and although Trump supported the investigation, prosecutors ended it last week to facilitate Warsh’s confirmation. Warsh’s nomination advanced in the Senate Banking Committee along party lines, marking the first time a Fed Chair was approved without bipartisan support. Other Fed tensions arose following the decision to leave rates unchanged during the April meeting. Three regional Presidents publicly disagreed with Powell, not on the most recent rate decision itself, but on the message that a rate cut is more likely than a hike. The three Presidents were effectively putting Warsh on notice that with rising energy prices, inflation near 3%, and ongoing tariffs, they do not believe the Fed can deliver the rate cuts sought by the White House. A fourth dissent expressed desiring a rate cut rather than keeping the rate unchanged. The four dissents at the April meeting were the most since 1992, before the Fed began announcing rate decisions in real time. The central bank’s next meeting is scheduled for June 16-17.

Sourcing for this section: The Wall Street Journal, “April’s Consumer Sentiment Is the Lowest on Record,” 4/24/2026; The Wall Street Journal, “Most Americans Think the Job Market Will Get Worse. Here’s Why That Matters.,” 4/24/2026; The Wall Street Journal, “Inflation Soared to 3.3% in March, Driven by Higher Gasoline Costs,” 4/10/2026; and The Wall Street Journal, “Powell Won’t Leave. The Fed Won’t Cut. Warsh Will Have to Deal With Both.,” 4/29/2026

Evolving Thoughtfully, Staying Disciplined,

Letting Trends Guide The Way

"To be a successful investor, you have to have a philosophy and process you believe in and can stick to, even under pressure."

—Howard Marks

The market environment in March and April presented a familiar but challenging pattern for investors in general and trend followers specifically: a sharp equity drawdown followed by an equally swift V-shaped recovery. Periods like these tend to expose the strengths — and weaknesses — of systematic investing approaches. For us, they have also served as a real-time validation of how our trend-following process has evolved over the years.

Historically, one of the common critiques of trend following is its tendency to lag during rapid reversals. A fast decline can trigger de-risking, only for markets to snap back before exposure is fully re-established. While that dynamic still exists to some degree in our portfolios because it is inherent in any rules-based, price-driven approach, our enhancements have meaningfully improved how we navigate both sides of that equation.

Refinement #1 – Using Single Stocks

One of the most important developments has been the refinement of how we express positions and exposures. When applicable and appropriate, we have embraced the deliberate use of individual securities rather than relying solely on market-capitalization-weighted ETFs. Broad ETFs, while efficient, can dilute the benefits of trend following by embedding exposure to both strong and weak components of the market. By focusing on single stocks, we are able to be more selective — leaning into leadership and avoiding areas showing persistent relative weakness.

During the March decline, this selectivity helped reduce exposure to the most vulnerable segments of the market. More importantly, as the recovery unfolded, it allowed us to reallocate toward stocks demonstrating the strongest momentum, rather than passively riding the entire index higher.

Refinement #2 – Expanding Alternatives Allocations

In parallel, we have expanded our use of alternatives trend- following allocations. These strategies, which may include non-traditional assets or differentiated signal constructions, provide an additional layer of diversification beyond equities. During periods of equity stress, they can behave differently — sometimes maintaining trends that are independent of the stock market’s direction.

In March, these allocations helped smooth the overall experience by providing exposure to trends that were either more stable or quicker to reassert themselves. As the equity market rebounded, they also contributed incremental return streams that complemented our core positioning.

Enhanced Adaptability

Taken together, we believe these enhancements have made our process more adaptive without sacrificing its core discipline. We are not attempting to predict turning points or outguess short-term market moves. Instead, we are continuously refining how we interpret and respond to price behavior. The goal is not perfection — no trend following system will capture every move — but rather, it is consistent improvement in how we manage risk and participate in opportunity.

The March episode is a good example of this progression in action. While the speed of both the decline and recovery tested all systematic investing approaches, our process was better equipped than in the past to navigate the volatility. By combining more robust signals, greater security-level selectivity, and diversified trend exposures, we were able to mitigate downside participation while remaining positioned to benefit as markets regained their footing.

Ultimately, this is the essence of our philosophy: evolve thoughtfully, stay disciplined, and let the trends — not predictions — guide the way forward.

April 2026 Investment Update:

A Disconnect Between Headlines & Market Behavior.

March 31, 2026

"The essence of investment management is the management of risks, not the management of returns."

—Benjamin Graham

Uncertainty can sometimes carry more weight than the event itself.

When headlines involve geopolitical tension or outcomes that are difficult to quantify, investor behavior often shifts quickly. Questions increase, confidence becomes more fragile, and long-term plans that felt stable weeks earlier can suddenly feel less certain.

Recent developments are a reminder of how quickly sentiment can change when visibility declines. The current environment is serious and evolving, but the underlying dynamic is not new. Markets have navigated wars, conflicts, and geopolitical shocks across decades, often experiencing short-term volatility while maintaining their longer-term trajectory.

This month’s Investment Update looks at how uncertainty shapes investor behavior, why markets often move ahead of the headlines, and how we are adjusting exposure in response to changing market conditions—not in anticipation of them.

But first, here’s a summary of the global asset classes utilized in our portfolios and their exposures for April.

Asset Allocation Update

Source: Blueprint Investment Partners

Adjustments can vary across strategies depending on each strategy's objectives. What's illustrated above most closely reflects allocation adjustments for the Growth Strategy. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility.

U.S. Equities

Exposure will decrease and move to underweight. The intermediate-term trend is now negative. The long-term trend remains positive.

International Equities

Exposure will decrease, with both foreign developed and emerging market equities now experiencing intermediate-term downtrends. Trends continue to be positive over the long-term timeframe.

Real Estate

Exposure will decrease back to the minimum allocation. With trends reverting back to negative status, it provides an opportunity to harvest losses while we await the next uptrend.

U.S. & International Treasuries

International Treasuries are now being partially expressed with an adaptive fixed income ETF. This will allow for an increase in exposure and offer the ability to potentially benefit from both positive and negative trends. However, U.S. Treasuries of medium to long duration are now in intermediate-term downtrends and exposure will decrease to underweight.

Alternatives

Exposure is expressed through a multi-asset alternative ETF. Fixed income maintains its top spot in terms of exposure, but will experience a flip from net long to net short. Net long equities is the next-largest exposure and the top net long position, but the magnitude of net long will decrease. International currencies and commodities will bring up the rear in terms of exposure, with both continuing to be net long.

Short-Term Fixed Income

Exposure will increase to overweight as it takes on exposure from weaker equities and fixed income.

Asset-Level Overview

Equities & Real Estate

After mostly flattening since last Halloween, U.S. equities succumbed to the uncertainty driven primarily by geopolitical events, producing its first downtrends in almost exactly a year. In 2025 the uncertainty was also political and internationally focused, but it was tariffs and not war. Now with missiles flying in the Middle East and no clear end in sight, investors are rattled, which is leaving markets flat to down.

If there is a bright spot amidst this volatility, it is that the U.S. economy appears strong outside of inflation pressure. In theory, this would support a favorable environment if and when the conflict in Iran comes to a sustainable conclusion. The challenge is that if history has taught us anything, it is that tensions in that part of the world can linger for a very long time.

Foreign developed and emerging market equities became the undisputed market leaders in late 2025 and were holding onto that spot for early 2026 until things escalated in Iran. Now with their greater reliance on Middle East oil and closer proximity, markets in those regions have generally given back all of their 2026 outperformance. Like their U.S. counterparts, they now have intermediate-term downtrends. With no stronger equity asset class for this exposure to land in our portfolios, we will drop it all the way down in our quality curve to the historically safest landing spot: cash equivalents.

Real estate securities had finally managed to break out of their long sideways pattern and develop what appeared to be sustainable uptrends. However, like the other equity assets, uncertainty abroad has led to a collapse in share prices, leading to a return of downtrends. The result is that short-term losses will be harvested systematically and exposure will return to its minimum.

Fixed Income & Alternatives

With input prices on the rise, inflation is back to being a real risk to the economy. The result is rising rates and falling bond prices, especially among higher, more sensitive duration instruments. Our systems will respond by harvesting losses and cutting exposure, returning these allocations to ultra-short-duration cash equivalents.

Within the alternatives allocation, the sudden rise in rates across the globe has pushed fixed income prices lower and produced many short positions within the portfolio. Across both domestic and international Treasuries, positions will move to net short. The rise in volatility will increase the number of short positions within equities, but not enough to keep it from being the largest long position. Strength in the U.S. Dollar has cut international currency long exposure in half, but it will still outpace commodities, where shorts in grains remain but longs in metals and energy continue to dominate.

3 Potential CatalystsFor Trend Changes

Diesel Prices: The average price of a gallon of diesel recently rose above $5.20 nationwide, about 40% higher than a month ago. Most of the states with the biggest price jumps are in the Southeast, especially South Carolina, where prices have risen 51% since February 21. Higher diesel and oil prices affect the cost of many goods, and these increases have an impact on core inflation. For most freight companies, a 40% jump in diesel prices means their overall costs go up by about 10%. Diesel is used to run equipment in fishing, farming, and construction, such as tractors and cranes. While consumers may not notice higher prices right away, these costs are already moving through the supply chain. Companies that ship fresh food are hit harder because their products need to be kept cold and delivered quickly. This likely means farmers will start charging wholesalers more, and retailers who rely on these products will raise prices for shoppers. Companies that ship goods with less urgent demand may wait to send shipments until prices drop or use trains, which take longer but use less diesel.

Housing Update: Mortgage rates have risen for the fourth week in a row, reaching their highest level since September. This sudden rise could slow down the start of the spring home-buying season. Freddie Mac reported that the average rate for a 30-year fixed mortgage is now 6.38%, up from 6.22%. Rates had dropped below 6% in late February for the first time since 2022, but have climbed quickly since then. The war in Iran and higher oil prices have led many to expect the Federal Reserve to keep short-term interest rates high for a while. This is tough news for the housing market, which has struggled for three years because of high prices and mortgage rates. Earlier this year, mortgage rates had fallen, and home prices were rising more slowly, giving buyers more choices and room to negotiate. Additionally, sales of existing homes went up in February as rates dropped. Zillow said that home-buying was more affordable in February than at any time since August 2022. However, as mortgage rates rise again, affordability is worsening, and the rapid increase may have scared off some buyers. The Mortgage Bankers Association said that mortgage applications have declined.

Consumer Services: Strong consumer spending is pushing up the prices of services like haircuts and healthcare, making this a key issue in the Federal Reserve’s efforts to control inflation. Over the past year, attention was mostly on rising prices for goods and, more recently, on higher gas prices due to the war with Iran. However, the cost of services is a big reason why inflation remains above the Fed’s 2% target. Economists say service prices keep rising because people still have money to spend. Real wages are higher, and unemployment is low. Stock market gains have also made wealthy Americans even wealthier. According to Eugenio Aleman, Chief Economist at Raymond James, high-income households spend a lot on services like flights and restaurant meals, which keeps service inflation high. Services now take up more retail space than stores selling goods. In February, service prices excluding housing rose 3.3% year over year, a bit slower than in previous months. In the 2010s, the average yearly increase was 2.1%. According to a study by the Urban Institute, health insurance premiums through the Affordable Care Act’s marketplaces rose 21.7% this year from 2025, which is a much faster increase than in past years. The rise is due to expiring credits, uncertainty among insurers, and higher healthcare costs.

Sourcing for this section: The Wall Street Journal, “$5 Diesel is Crushing Truckers. It Will Soon BeFelt Across the Economy.,” 3/22/2026; The Wall Street Journal, “Mortgage Rates Rise for Fourth Straight Week,” 3/26/2026; and The Wall Street Journal, “America’s Sneaky Inflation Culprit: Manicures, Haircuts and Doggy Daycare,” 3/23/2026

Emotional Investor Reactions Are Usually Riskier

Than Perceived ‘Risky’ Events

"Far more money has been lost by investors preparing for corrections, or anticipating corrections, than has been lost in corrections themselves."

—Peter Lynch

Markets don’t operate in a vacuum. Headlines matter — especially when they involve war, geopolitical tension, or uncertainty that feels difficult to quantify. And if there’s one thing we’ve been reminded of time and again, it’s that uncertainty — not necessarily the event itself — is what tends to unsettle investors the most. When geopolitical conflict escalates, the instinctive reaction is often fear. Clients call. Long-term plans suddenly feel less certain. The narrative becomes, “This time is different!”

But as we discuss in our most recent blog, history suggests otherwise.

Markets have endured wars, conflicts, and geopolitical shocks across decades. While short-term volatility is common, the long-term trajectory has often remained intact. In many cases, markets begin recovering well before the underlying conflict is resolved. That disconnect — between headlines and market behavior — is where many investors get tripped up. The real risk is often not the event itself, but the behavioral response to it.

Avoiding uncertainty may feel prudent, but without a plan for how to do so it may lead to jumping the ship too early or missing the recovery that follows. And that recovery rarely comes with a clear signal that “it’s safe to get back in.” By the time uncertainty fades, markets have frequently already moved higher to a point making the re-entry emotionally difficult.

That said, acknowledging history doesn’t mean ignoring risk. This is where investing process matters. Rather than trying to predict geopolitical outcomes — or guess how markets will react — our firm relies on a disciplined, trend-following approach. Trends allow us to observe what markets are actually doing, not what we think they should do. When uncertainty rises and trends deteriorate, our investing process naturally reduces exposure to risk assets. You see this playing out in real time, as we are reducing U.S. equities exposure due to deteriorating trends heading into April.

Importantly, this is not about reacting to headlines. It’s about responding to price behavior. As trends weaken, we systematically reduce exposure. Not because of any single event, but because the market itself is signaling increased risk. We think this approach helps us avoid making emotionally driven decisions in moments when emotions are running high.

The other side of this discipline is just as important. We remain equally prepared to add exposure back. If uncertainty begins to abate and markets rebound, trends will reflect that improvement. And when they do, our systematic investing process allows us to increase exposure again — without hesitation and without needing to “feel comfortable” first.

This is one of the key advantages of a rules-based approach, in our view. It removes the burden of prediction and replaces it with a repeatable framework for decision-making. In environments like today, that matters. Because the reality is that uncertainty is always present. War may dominate headlines today; tomorrow it could be inflation, central banks, or something entirely unexpected. The specific catalyst changes, but the underlying challenge for investors remains the same: how to stay disciplined when uncertainty is high.

Our answer is simple. We don’t try to predict. We don’t react emotionally. And we don’t assume that “this time is different.” And throughout, our goal remains consistent: to participate in markets when conditions are favorable and to step back when risks increase. History doesn’t eliminate uncertainty — but it does provide perspective. We think investing process turns that perspective into action.